An underwriter is a financial expert who takes a look at your finances and assesses how much risk a lender will take on if they decide to give you a loan. More specifically, underwriters evaluate your credit history, assets, the size of the loan you request and how well they anticipate that you can pay back your loan.

What role does an underwriter play in the mortgage application process quizlet?

the underwriter is the last person who is in a position to protect the investor. -The underwriter’s job is to approve or deny the loan and, because of this, the underwriter needs the highest level of expertise possible.

Does the underwriter have the final say?

Underwriters Have Final Say They make sure that all of the tax, title, insurance and closing documentation is in place. … Oftentimes an underwriter’s denial can be appealed to the head underwriter or other superior, but the facts must be in place to support any overturn of an underwriter’s decision.

Do all mortgage applications go to underwriters?

No, not all mortgage applications go to underwriters but this depends greatly on the mortgage lender and their specific underwriting process.Does underwriter give pre approval?

The underwriter reviews all your documentation to get pre-approved (just like in the traditional loan process), but they do it upfront — hence the name. This process is much quicker than traditional underwriting, which can sometimes take weeks of back-and-forth between you and your lender.

What is a mortgage underwriting quizlet?

Mortgage Underwriting. Process by which a lender determines the terms and amount of a loan by looking at the credit of the borrower and the level of risk that the borrower poses to the lender.

What does the underwriter do quizlet?

The underwriter must ensure that the property is eligible and meets lender guidelines for collateral. … The underwriter will be looking at the location of the subject property and any possible hazards or deficiencies that may affect the marketability of the property if the lender should have to foreclose.

How do you know when your mortgage loan is approved?

How do you know when your mortgage loan is approved? Typically, your loan officer will call or email you once your loan is approved. Sometimes, your loan processor will pass along the good news.Is no news good news in underwriting?

When it comes to mortgage lending, no news isn’t necessarily good news. … Particularly in today’s economic climate, many lenders are struggling to meet closing deadlines, but don’t readily offer up that information.

How often do mortgages get denied in underwriting?One in every 10 applications to buy a new house — and a quarter of refinancing applications — get denied, according to 2018 data from the Consumer Financial Protection Bureau.

Article first time published onWhat should you not do during underwriting?

Tip #1: Don’t Apply For Any New Credit Lines During Underwriting. Any major financial changes and spending can cause problems during the underwriting process. New lines of credit or loans could interrupt this process. Also, avoid making any purchases that could decrease your assets.

What is red flag in mortgage?

The biggest mortgage fraud red flags relate to phony loan applications, credit documentation discrepancies, appraisal and property scams along with loan package fraud. … With mortgage fraud so rampant, it’s vital for both real estate and financial professionals to know how to spot warning signs.

What comes after underwriting?

Once your loan goes through underwriting, you’ll either receive final approval and be clear to close, be required to provide more information (this is referred to as “decision pending”), or your loan application may be denied.

Can you talk to the underwriter?

Underwriters Cannot Directly Ask You Anything It is important to note that underwriters should not be in actual contact with you. All questions and discussions should be handled through your lender or loan officer. An underwriter talking to you directly, or even knowing you personally, is a conflict of interest.

What is the difference between preapproved and approved?

A pre-approval is a non-binding statement saying, based on a cursory review of your unverified financial status, that you are eligible for a loan up to a certain amount. … The approval is the process of obtaining a specific loan on a specific property for a specific amount.

What do the underwriters look for?

When trying to determine whether you have the means to pay off the loan, the underwriter will review your employment, income, debt and assets. They’ll look at your savings, checking, 401k and IRA accounts, tax returns and other records of income, as well as your debt-to-income ratio.

What do underwriters use to determine how much they are willing to loan on a given property based on its value?

Underwriters are financial experts employed by lending companies. … Then, they decide how much risk they’re willing to take based on an individual’s financial profile. To evaluate how much (or how little) risk an applicant presents, underwriters look at the three Cs: credit, capacity and collateral.

What are the primary objectives of closing?

Closing entries are very important parts of the accounting cycle. Their purpose is to clear out balances in temporary accounts by transferring them to permanent accounts. Temporary accounts are accounts that are only used for a specific time period, usually one accounting period.

What is not typically included in a building's specifications?

What is not typically included in a building’s specifications? A specific selling price which the property will be listed at when completed. bearing walls.

What does balloon mean in a loan?

A balloon payment is a larger-than-usual one-time payment at the end of the loan term. If you have a mortgage with a balloon payment, your payments may be lower in the years before the balloon payment comes due, but you could owe a big amount at the end of the loan.

What is bubble loan?

In this type of loan with no balloon payment, his/her entire loan will be amortised in small monthly payments till the time his/her entire loan is paid. If there is balloon payment involved then, usually, the entire principal payment is paid in lump sum towards the end of the term.

What type of loan has a term that is shorter than the amortized period?

Frequently, banks offer loans where the term is shorter than amortization. When the two are not coterminous, the loan is said to have a balloon–common parlance for the remaining principal owed at the end of the term.

Can you be denied in underwriting?

Even if you are pre-approved, your underwriting can still be denied. … Your loan is never fully approved until the underwriter confirms that you are able to pay back the loan. Underwriters can deny your loan application for several reasons, from minor to major.

How long does it take for the underwriter to make a decision?

Under normal circumstances, initial underwriting approval happens within 72 hours of submitting your full loan file. In extreme scenarios, this process could take as long as a month. However, it’s unlikely to take so long unless you have an exceptionally complicated loan file.

Why is underwriter taking so long?

Underwriters often request additional documents. This is when the mortgage lender’s underwriter (or underwriting department) reviews all paperwork relating to the loan, the borrower, and the property being purchased. … It’s another reason why mortgage lenders take so long to approve loans.

Why would a mortgage be declined?

These are some of the common reasons for being refused a mortgage: You’ve missed or made late payments recently. You’ve had a default or a CCJ in the past six years. You’ve made too many credit applications in a short space of time in the past six months, resulting in multiple hard searches being recorded on your …

How long does it take for underwriter to clear to close?

Clear To Close: At Least 3 Days Once the underwriter has determined that your loan is fit for approval, you’ll be cleared to close. At this point, you’ll receive a Closing Disclosure.

Can I be denied mortgage loan at closing?

Can a mortgage loan be denied after closing? Though it’s rare, a mortgage can be denied after the borrower signs the closing papers. For example, in some states, the bank can fund the loan after the borrower closes. “It’s not unheard of that before the funds are transferred, it could fall apart,” Rueth said.

Do underwriters look at spending habits?

Banks check your credit report for outstanding debts, including loans and credit cards and tally up the monthly payments. … Bank underwriters check these monthly expenses and draw conclusions about your spending habits.

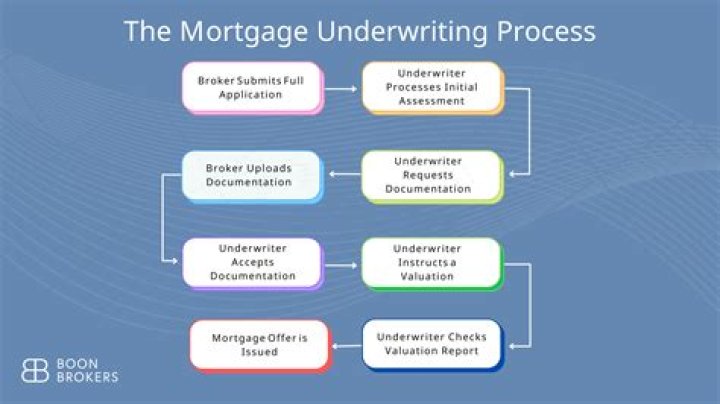

How do you pass the underwriting process?

- Step 1: Apply for the mortgage. …

- Step 2: Receive the loan estimate from your lender. …

- Step 3: Get your loan processed. …

- Step 4: Wait for your mortgage to be approved, suspended or denied. …

- Step 5: Clear any loan contingencies. …

- Step 6: Close on your house.

How often does mortgage financing fall through?

Relax — just not too much. You read earlier that 3.9 percent of residential property transactions fail. That means 96.1 percent succeed. And, by the time the closing table is in sight, your chances are already much better.