Cost Volume-Profit (CVP) relationship is an analysis which studies the relationships between the following factors and its impact on the amount of profits. … In simple words, CVP is a management accounting tool that expresses relationship among total sales, total cost and profit.

What is the relationship between the cost volume and profit?

Cost-volume-profit (CVP) analysis is a way to find out how changes in variable and fixed costs affect a firm’s profit. Companies can use CVP to see how many units they need to sell to break even (cover all costs) or reach a certain minimum profit margin.

What is the CVP formula?

The key CVP formula is as follows: profit = revenue – costs. … You can then convert that number into a percentage by dividing it by your revenue again and multiplying by 100. This gives you the contribution margin ratio or the profit-volume ratio. Your costs ratio can also be used to work out your break-even sales units.

Why is cost volume profit relationship important in business management?

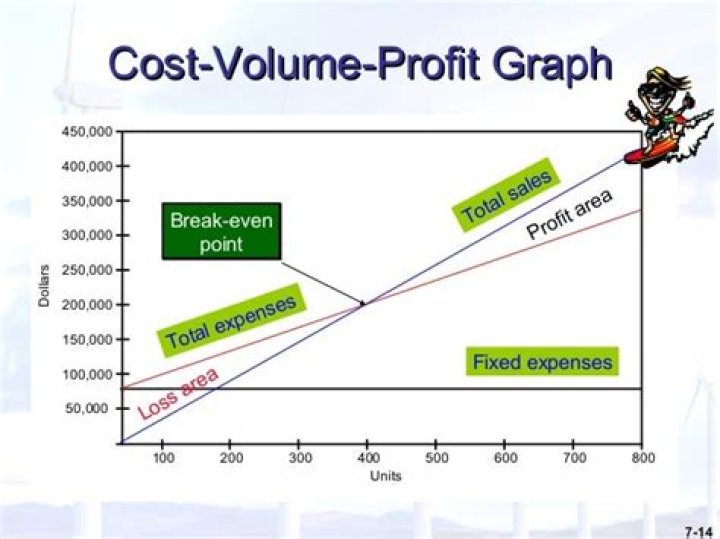

The relationship between cost, volume and profit makes up the profit structure of an enterprise. … As a starting point in profit planning, it helps to determine the maximum sales volume to avoid losses, and the sales volume at which the profit goal of the firm will be achieved.What is cost volume ratio?

When calculated as a ratio, it is the percent of sales dollars available to cover fixed costs. Once fixed costs are covered, the next dollar of sales results in the company having income. The contribution margin is sales revenue minus all variable costs. It may be calculated using dollars or on a per unit basis.

What is CVP and break-even analysis?

Cost Volume Profit (CVP) Analysis, also known as break-even analysis, is a financial planning tool that leaders use when determining short-term strategies for their business. This conveys to business decision-makers the effects of changes in selling price, costs, and volume on profits (in the short term).

How do costs and volume affect profit?

Assuming your sales exceed your variable costs, each additional unit of sales volume increases your gross profits and your net income. If you can lower your costs without impacting revenue and maintain the same sales volume, your profits will go up.

How does CVP help in decision making?

The CVP analysis is aimed at determining the output that adds value to the business, emphasizes the impact of fixed costs, break-even points, target profits that determine sales volume and revenue estimates. Making price decisions and price structures is simpler when using the CVP analysis.What are the benefits of using cost volume profit analysis?

Cost Volume Profit analysis or CVP analysis helps in identifying the operating activity levels with a purpose to avoid any kind of losses and achieve profits. Moreover, it also helps the companies to plan their future operations and see whether their organizational performance is going on the right track or not.

What are the objectives of cost volume profit analysis?The main objective of the cost-volume-profit analysis is to help management make important decisions revealing the interrelationship among the volume of output and sales, cost, and profit.

Article first time published onWhat are the basic components of cost volume profit CVP analysis?

The components of CVP analysis are: Level or volume of activity. Unit selling prices. Variable cost per unit.

What are the components of cost volume profit CVP analysis?

Components of CVP Analysis CM ratio and variable expense ratio. Break-even point (in units or dollars) Margin of safety. Changes in net income.

How do costs affect profit?

Fixed costs are expenses that do not change based on production levels; variable costs are expenses that increase or decrease according to the number of items produced. Both fixed and variable costs have a large impact on gross profit—an increase in expenses to produce goods means lower gross profit.

How does cost vary with volume?

Understanding Variable Costs As the volume of production and output increases, variable costs will also increase. Conversely, when fewer products are produced, the variable costs associated with production will consequently decrease.

What is cost-volume-profit analysis and what are its assumptions What is its significance to the management?

Cost-volume-profit analysis (CVP analysis) helps a business in planning and decision-making. It provides information on how profits and costs are affected by changes in volume or level of activity. CVP analysis assumes the following: Costs are segregated into purely fixed and purely variable.

How is CVP analysis used in pricing?

- Sum fixed costs. Tally your company’s fixed costs: …

- Determine the product’s selling price. …

- Calculate the variable cost per unit. …

- Calculate the unit CM and CM ratio. …

- Complete the CVP analysis.

What is meant by cost volume profit analysis explain its application in managerial decision making How would you construct a break even chart?

Cost Volume Profit Analysis (CVP) looks at the impact on the operating profit due to the varying levels of volume and the costs and determines a break-even point for cost structures with different sales volumes that will help managers in making economic decisions for short term.

What are the 3 elements of CVP analysis?

The point of a CVP analysis is to determine how changes in variable and fixed costs will affect profits. What are the three elements of cost-volume-profit analysis? The three main elements are cost, sales volume and price. A CVP analysis looks at how these elements influence profit.

What is the relationship between cost and production function?

There is an inverse relationship between production and costs. The harder it is to produce something, for example, the more labor it takes, the higher the cost of producing it, and vice versa.

How is cost important in a business?

Understanding your costs is vital for informed business decisions. It helps you determine the profitability of your operations and how to set prices. … “If you don’t know your costs accurately and in a timely way, it’s very hard to make well-informed decisions about your operations.”

What is expensive profit accounting?

Accounting profit shows the amount of money left over after deducting the explicit costs of running the business. Something that seems to cost a great deal is “expensive”.

What is volume in cost accounting?

The cost volume formula is used to derive the total cost that will be incurred at certain production volumes. The formula is useful for deriving total costs for budgeting purposes, or to identify the approximate profit or loss levels likely to be achieved at certain sales volumes. The cost volume formula is: Y = a + bx.

How is volume cost calculated?

Cost per unit of volume (cubic unit) can be obtained by multiplying the dimensions (to get the volume of a rectangular parallelepiped) and dividing the result by cost of strip.

What type of cost remains the same as the volume changes?

Cost 2 is a fixed cost because as the number of units produced changes, total costs remain the same and per unit costs change.