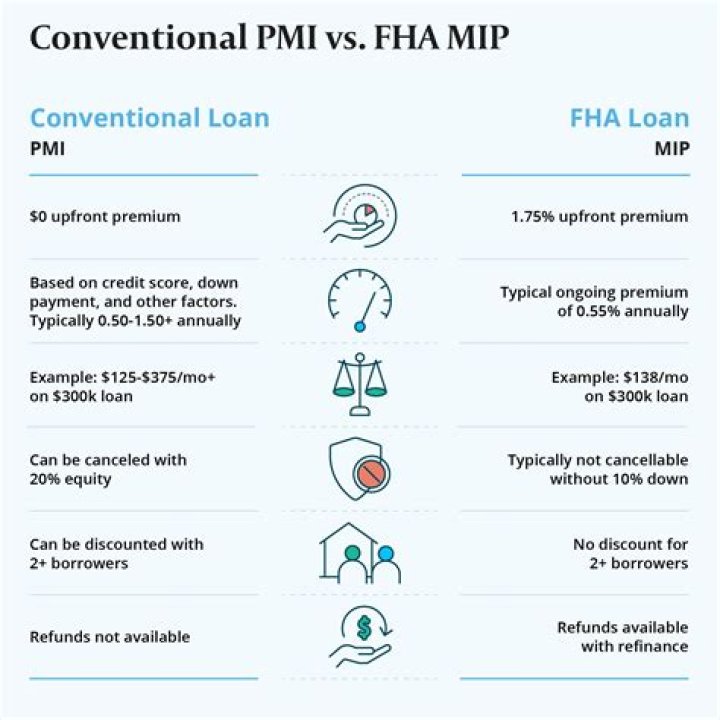

Borrowers with conventional loans must purchase private mortgage insurance, or PMI, from a company selected by their lender. … A conventional loan without PMI, then, is one where the lender was satisfied with the borrower’s down payment and didn’t require private mortgage insurance.

What conventional loans dont require PMI?

USDA loans don’t require borrowers to pay private mortgage insurance (PMI), but they do require borrowers to pay a guarantee fee, which is similar to PMI. If you pay it upfront, the fee is 1% of the total loan amount. You also have the option to pay the guarantee fee as part of your monthly payment.

Do conventional loans carry PMI?

Lower Mortgage Insurance Premiums Don’t confuse this with private mortgage insurance (PMI), which is applicable only to conventional loans. Conventional loans require a 5% down payment. PMI can be removed once loan-to-value ratio (LTV) reaches 80%. Unlike PMI, MIP lasts for the life of the loan.

How can I avoid PMI without 20% down?

The first way is to look for a lender offering lender–paid mortgage insurance (LPMI), which eliminates PMI in exchange for a higher interest rate. Second, buyers can opt for a piggyback mortgage – one that uses a second loan to cover part of the down payment and reach 20%, therefore bypassing the PMI requirement.How can I avoid PMI on a conventional loan?

One way to avoid paying PMI is to make a down payment that is equal to at least one-fifth of the purchase price of the home; in mortgage-speak, the mortgage’s loan-to-value (LTV) ratio is 80%. If your new home costs $180,000, for example, you would need to put down at least $36,000 to avoid paying PMI.

Is it better to put 20 down or pay PMI?

PMI is designed to protect the lender in case you default on your mortgage, meaning you don’t personally get any benefit from having to pay it. So putting more than 20% down allows you to avoid paying PMI, lowering your overall monthly mortgage costs with no downside.

What is a good credit score for a conventional loan?

Conventional Loan Requirements It’s recommended you have a credit score of 620 or higher when you apply for a conventional loan. If your score is below 620, you might be offered a higher interest rate.

How can I avoid PMI with 5% down?

The traditional way to avoid paying PMI on a mortgage is to take out a piggyback loan. In that event, if you can only put up 5 percent down for your mortgage, you take out a second “piggyback” mortgage for 15 percent of the loan balance, and combine them for your 20 percent down payment.Is PMI based on credit score?

Credit scores and PMI rates are linked Insurers use your credit score, and other factors, to set that percentage. A borrower on the lowest end of the qualifying credit score range pays the most. “Typically, the mortgage insurance premium rate increases as a credit score decreases,” Guarino says.

How long is PMI required on a conventional loan?That means you will have to wait at least two years before being able to get rid of your mortgage insurance. Check current mortgage rates.

Article first time published onDo conventional loans require MIP?

Conventional loans do not have upfront mortgage insurance premiums. Another important difference between MIP and PMI are the monthly insurance premiums. Every person who buys a house with an FHA loan must also pay monthly insurance premiums (MIP).

How long do you have to keep PMI on a conventional loan?

The servicer also must stop the PMI at the halfway point of your amortization schedule. For example, if you have a 30-year loan, the midpoint would be after 15 years. If you have a 15-year loan, the halfway point is 7.5 years.

Is PMI required by law?

Borrower paid mortgage insurance (BPMI) means PMI is required for a residential mortgage transaction, the payments for which are made by the borrower.

Is PMI based on appraisal or purchase price?

When it comes to calculating mortgage insurance or PMI, lenders use the “Purchase price or appraised value, whichever is less” guideline. Thus, using a purchase price of $200,000 and $210,000 appraised value, the PMI rate will be based on the lower purchase price.

What happens if you don't put 20 down on a house?

What happens if you can’t put down 20%? If your down payment is less than 20% and you have a conventional loan, your lender will require private mortgage insurance (PMI), an added insurance policy that protects the lender if you can’t pay your mortgage.

Is Conventional better than FHA?

FHA loans allow lower credit scores than conventional mortgages do, and are easier to qualify for. Conventional loans allow slightly lower down payments. … FHA loans are insured by the Federal Housing Administration, and conventional mortgages aren’t insured by a federal agency.

Can you put 3 down on a conventional loan?

Can I get a mortgage with 3% down? Yes! The conventional 97 program allows 3% down and is offered by many lenders. Fannie Mae’s HomeReady loan and Freddie Mac’s Home Possible loan also allow 3% down with extra flexibility for income and credit qualification.

Can you pay off a conventional loan early?

A mortgage prepayment penalty is a fee that some lenders charge when you pay all or part of your mortgage loan term off early. The penalty fee is an incentive for borrowers to pay back their principal slowly over a full term, allowing mortgage lenders to collect interest.

Does PMI go towards principal?

Private mortgage insurance does nothing for you This is a premium designed to protect the lender of the home loan, not you as a homeowner. Unlike the principal of your loan, your PMI payment doesn’t go into building equity in your home.

What is a conventional loan for a house?

A conventional loan is a mortgage loan that’s not backed by a government agency. Conventional loans are broken down into “conforming” and “non-conforming” loans. … However, some lenders may offer some flexibility with non-conforming conventional loans.

How much should I put down on a 200k house?

Conventional mortgages, like the traditional 30-year fixed rate mortgage, usually require at least a 5% down payment. If you’re buying a home for $200,000, in this case, you’ll need $10,000 to secure a home loan. FHA Mortgage. For a government-backed mortgage like an FHA mortgage, the minimum down payment is 3.5%.

How much is PMI on a $100 000 mortgage?

While PMI is an initial added cost, it enables you to buy now and begin building equity versus waiting five to 10 years to build enough savings for a 20% down payment. While the amount you pay for PMI can vary, you can expect to pay approximately between $30 and $70 per month for every $100,000 borrowed.

Is PMI tax deductible?

A PMI tax deduction is only possible if you itemize your federal tax deductions. … The standard deduction for 2020 was $12,400 for single taxpayers or $24,800 for married couples filing jointly, and it’s increasing to $12,550 for single filers and $25,100 for couples for the 2021 tax year.

How do you calculate if PMI can be removed?

Pay Down Your Mortgage One way to get rid of PMI is to simply take the purchase price of the home and multiply it by 80%. Then pay your mortgage down to that amount. So if you paid $250,000 for the home, 80% of that value is $200,000. Once you pay the loan down to $200,000, you can have the PMI removed.

Will banks waive PMI?

The lender will waive PMI for borrowers with less than 20 percent down, but also bump up your interest rate, so you need to do the math to determine if this kind of loan makes sense for you. Some government-backed programs don’t charge mortgage insurance.

Is PMI tax deductible in 2021?

Taxpayers have been able to deduct PMI in the past, and the Consolidated Appropriations Act extended the deduction into 2020 and 2021. The deduction is subject to qualified taxpayers’ AGI limits and begins phasing out at $100,000 and ends at those with an AGI of $109,000 (regardless of filing status).

Do credit unions waive PMI?

Zillow notes that credit unions will occasionally waive PMI for applicants on a case-by-case basis. Some financial institutions will also ask buyers with poor credit or inconsistent income to get PMI, even if they make a significant down payment.

Is a conventional loan good or bad?

Is a Conventional Loan Good? A conventional loan can be a good choice, depending on your financial situation. Generally, conventional loans are best for buyers of homes under $500,000, and if you have good credit, you will qualify for the lowest possible interest rates, says David J.

Can a conventional loan be Fannie Mae?

Conventional loans are also called conforming loans because they conform to Fannie Mae and Freddie Mac standards. Fannie Mae and Freddie Mac are government-created enterprises that buy mortgages from lenders and hold the mortgages or turn them into mortgage-backed securities.

Does MIP go away?

Depending on your down payment, and when you first took out the loan, FHA MIP usually lasts 11 years or the life of the loan. MIP will not fall off automatically. To remove it, you’ll have to refinance into a conventional loan once you have enough equity.

Is it hard to get a conventional home loan?

Even though a conventional loan is the most common mortgage, it is surprisingly difficult to get. Borrowers need to have a minimum credit score of about 640 in order to qualify—the highest minimum score of all mortgage products—and have a debt-to-income ratio of 43% or less.