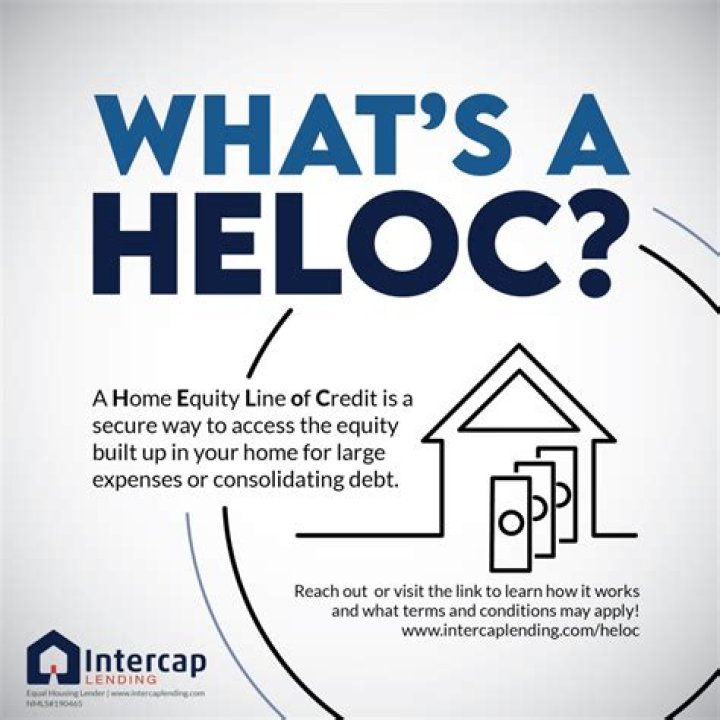

A home equity line of credit, also known as a HELOC, is a line of credit secured by your home that gives you a revolving credit line to use for large expenses or to consolidate higher-interest rate debt on other loans 1 such as credit cards.

What is a purchase money HELOC?

A HELOC (also known as a second mortgage or junior mortgage) is taken out from your home after you have purchased your home. A purchase money 2nd loan is a 2nd loan that was used to buy your home. It is not a line of credit that was taken out after you bought your home.

What happens if you don't use your HELOC?

Though HELOCs carry lower interest rates than credit cards, they are still borrowed money. You eventually must repay the HELOC, and the more you borrowed and used, the larger your payments will be. If you don’t, the lender will foreclose.

What is a HELOC in simple terms?

A HELOC — also known as a home equity line of credit — allows you to borrow against the equity you’ve already built up in your home. As a line of credit, a HELOC allows for flexibility around both borrowing and repaying money.What does purchase money 2nd mean?

What is a Purchase Money Second Mortgage Loan? A Purchase Money Second Loan can be used by those who are looking to purchase a home and are interested in a second mortgage to supplement the amount of down payment needed.

What are the disadvantages of a home equity line of credit?

- HELOCs can come with a minimum withdrawal amount.

- There can be limitations to how you access the funds.

- There is a set withdraw period after which you cannot access any further funds.

- There can be fees associated with a HELOC.

- You can hurt your credit if you do not make payments on time.

- Harder to qualify right now.

Is an appraisal required for a HELOC?

Is an appraisal required with a HELOC? In general, a new appraisal will be required to qualify for a home equity line of credit. … However the lender determines a current home value, it’s needed to calculate the amount of credit you’ll be eligible to borrow.

Can you pay off HELOC early?

At any time, you can pay off any remaining balance owed against your HELOC. … If you pay off your HELOC balance early, your lender may offer you the choice to close the line of credit or keep it open for future borrowing. Why you should close a HELOC. Sometimes, a lender will charge annual fees for open lines of credit.How much equity can you borrow from your house?

Depending on your financial history, lenders generally want to see an LTV of 80% or less, which means your home equity is 20% or more. In most cases, you can borrow up to 80% of your home’s value in total. So you may need more than 20% equity to take advantage of a home equity loan.

How is a HELOC paid back?HELOC repayment Typically, you’re only required to make interest payments during the draw period, which tends to be 10 to 15 years. You can also make payments back toward the principal during the draw period. When you pay off part of the principal, those funds go back to your line amount.

Article first time published onWhat does Dave Ramsey say about HELOC?

Dave Ramsey advises his followers to avoid home equity loans and HELOCs. Although it might seem like home equity loans might make sense if homeowners are trying to quickly pay down credit card debt in their quest to become debt-free, he still does not recommend home equity debt.

Can I sell my home if I have a HELOC?

Except for short sales, mortgage, HELOC and other lien holders normally don’t interfere with their borrowers’ home sales. … If you sell your home and will be paying off any liens at least partially on your own, you’ll need to bring funds to the sale’s closing.

Does your HELOC have to be with same bank as mortgage?

You don’t have to go with the same company that handles your mortgage. It generally pays to shop around to try to get the best rate and all-in cost. When thinking about the total costs, consider the principal amount you must repay and the interest cost, as well as other fees.

What is a PM2 loan?

A Purchase Money Second (PM2) Home Loan* is a second mortgage that closes with a corresponding first mortgage from the same lender. The first mortgage covers 80% of the home value and the second mortgage (a fixed-rate home equity loan) covers 10% – meaning you have a down payment of only 10%.

What does table Fund mean?

Table funding means a settlement at which a loan is funded by a contemporaneous advance of loan funds and an assignment of the loan to the person advancing the funds.

What is a piggyback loan?

A piggyback loan involves taking out two mortgages, one large and one small. The smaller mortgage “piggybacks” on the larger one. … The other is a home equity loan or home equity line of credit. The main reason to take out a piggyback loan is to avoid paying for private mortgage insurance.

Are there closing costs on a HELOC?

HELOC closing costs Closing costs for a HELOC are often a bit lower than the costs of closing a primary mortgage, but the average closing costs for a home equity loan or line of credit (depending on the lender and the loan product) can add up to between 2 percent and 5 percent of your total loan cost.

Does unused HELOC affect credit score?

Do Unused Credit Lines Hurt Your Credit Score? Unused lines of credit typically improve your utilization rate, which would improve your credit score. However, HELOCs are a type of revolving credit, just like a credit card.

How long does it take to get money from HELOC?

The truth is that home equity loan approval can take anywhere from a week—or two up to months in some cases. Most lenders will tell you that the average window of time it takes to get a home equity loan is between two and six weeks, with most closings happening within a month.

What scenario do most homeowners use the equity in their home?

Homeowners sometimes use home equity to pay off other personal debts, such as car loans or credit cards. “This is another very popular use of home equity, as one is often able to consolidate debt at a much lower rate over a longer-term and reduce their monthly expenses significantly,” Hackett says.

What should you do if you start having a hard time paying your mortgage?

- Refinance.

- Get a loan modification.

- Work out a repayment plan.

- Get forbearance.

- Short-sell your home.

- Give your home back to your lender through a “deed-in-lieu of foreclosure”

Is a second mortgage a home equity loan?

A second mortgage is a secured loan (like a home equity loan or home equity line of credit) that you take out using the equity you’ve accumulated in your home without having to refinance your existing mortgage.

What is the monthly payment on a $100 000 home equity loan?

Assuming principal and interest only, the monthly payment on a $100,000 loan with an APR of 3% would come out to $421.60 on a 30-year term and $690.58 on a 15-year one. Credible is here to help with your pre-approval.

What is the payment on a 50000 home equity loan?

Loan payment example: on a $50,000 loan for 120 months at 3.80% interest rate, monthly payments would be $501.49.

What is the monthly payment on a $200 000 home equity loan?

On a $200,000, 30-year mortgage with a 4% fixed interest rate, your monthly payment would come out to $954.83 — not including taxes or insurance.

What is minimum payment on HELOC?

Your minimum monthly payment is $50, consider making an additional principal payment to reduce your interest. Apply for a HELOCCompare rates. Total. Yearly. Ending balance.

Can I use my HELOC for anything?

Like a home equity loan, a HELOC can be used for anything you want. However, it’s best-suited for long-term, ongoing expenses like home renovations, medical bills or even college tuition. … A HELOC usually has a variable interest rate based on the fluctuations of an index, such as the prime rate.

Are HELOC loans amortized?

HELOC loans are not fully amortized. They only allow you to make interest-only payments during the period of the draw.

How do I pay off my HELOC?

- Understand HELOC Payments. A HELOC has two separate periods; the draw period and repayment period. …

- Increase Your Monthly Payments. …

- Explore Refinancing Options.

What is the danger of putting up collateral for a loan?

The biggest risk of a collateral loan is you could lose the asset if you fail to repay the loan. It’s especially risky if you secure the loan with a highly valuable asset, such as your home. It requires you to have a valuable asset.

Why is a second mortgage bad?

Second mortgages are riskier to lenders than first mortgages. That’s because in a foreclosure sale, the first mortgage gets paid off first. The second mortgage may not be completely repaid from the proceeds of the sale. Second mortgages are cheaper than most other loans because they are secured by real estate.