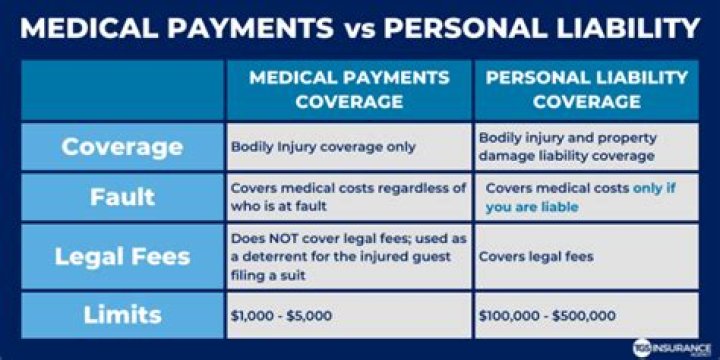

Another type of personal liability coverage typically included with your homeowners policy is for medical payments to others. Typically, a homeowners, renters or condo policy provides for the payment of necessary medical expenses for persons who are accidentally injured on your property.

Does liability home protection cover medical expenses?

Liability protection Liability covers you against lawsuits for bodily injury or property damage that you or family members cause to other people. … It does not, however, pay the medical bills for your own family or your pet.

What does Medical payments cover on home insurance?

Medical payments coverage can help to pay for expenses related to an injury that occurs on your property — whether you’ve been found liable or not. It works by reimbursing the policyholder for expenses that have been paid out to things like medical bills and funeral costs that are derived from the injury.

Does homeowners insurance cover medical accidents?

Does homeowners insurance cover personal injury? Homeowners insurance covers personal injuries as long as your policy includes personal liability coverage, and most policies do. … Furthermore, your personal liability insurance only applies to others, while any injuries of your own would be covered under health insurance.What does homeowners insurance cover and not cover?

Typical homeowners insurance policies offer coverage for damage caused by fires, lightning strikes, windstorms and hail. … For example, damage caused by earthquakes and floods are not typically covered by homeowners insurance.

Does home insurance cover damage to other people's property?

Homeowners insurance is a package policy. This means that it covers both damage to property and liability or legal responsibility for any injuries and property damage policyholders or their families cause to other people.

Does homeowners insurance cover the homeowner?

What Is Homeowners Insurance? Homeowners insurance is a form of property insurance that covers losses and damages to an individual’s residence, along with furnishings and other assets in the home. Homeowners insurance also provides liability coverage against accidents in the home or on the property.

What is covered under medical payments to others?

Medical payments coverage is reserved for cheaper hospital and doctor bills, such as X-rays, ambulance rides, physical therapy, medication, deductibles and various other small medical bills that usually remain after health insurance picks up its portion.What is not protected by most homeowners insurance?

Termites and insect damage, bird or rodent damage, rust, rot, mold, and general wear and tear are not covered. Damage caused by smog or smoke from industrial or agricultural operations is also not covered. If something is poorly made or has a hidden defect, this is generally excluded and won’t be covered.

Which of the following homeowners coverage does not have a deductible?Which of the following homeowners coverage does not have a deductible? Damage to property of Others is an Additional Coverage under Section II, which is not subject to a deductible. A guest falls in K’s house and is injured in an amount of $1,000.

Article first time published onWhat are the six categories typically covered by homeowners insurance?

Generally, a homeowners insurance policy includes at least six different coverage parts. The names of the parts may vary by insurance company, but they typically are referred to as Dwelling, Other Structures, Personal Property, Loss of Use, Personal Liability and Medical Payments coverages.

Does home insurance cover roof leaks?

Homeowners insurance may cover a roof leak if it is caused by a covered peril. Suppose your roof is damaged by fire, hail or wind. … However, homeowners insurance generally does not cover damage resulting from lack of maintenance or wear and tear. Instead, it typically helps pay to repair sudden, accidental damage.

What can invalidate house insurance?

- Leaving your home unoccupied. …

- Not getting in touch when something changes. …

- Keeping quiet about an incident (even the really small ones) …

- Using your home for business. …

- Getting a lodger. …

- Having your home renovated. …

- Inflating the value of your contents.

What are the 3 basic levels of coverage that exist for homeowners insurance?

Homeowners insurance policies generally cover destruction and damage to a residence’s interior and exterior, the loss or theft of possessions, and personal liability for harm to others. Three basic levels of coverage exist: actual cash value, replacement cost, and extended replacement cost/value.

Do I need homeowners insurance if I own my home?

If you own your home outright (meaning you’ve paid off your mortgage completely), you aren’t legally required to have homeowners insurance. … Your mortgage lender will likely require proof of insurance before closing. The amount you’ll need to be insured for will vary but is typically the balance of your loan or higher.

Will homeowners insurance cover sagging floors?

Will homeowners insurance cover sagging floors? … As long as the damage was caused by a danger specified in the insurance policy for homeowners, the insurer will pay to replace your floors. If you are uncertain whether you are covered, speak to an experienced house insurance attorney.

What does liability insurance protect?

Generally speaking, it helps pay to repair another person’s property or for their medical bills if the policyholder is found responsible for causing the damage or injuries. If you’re at fault for an accident that injures another person, bodily injury liability coverage helps pay for their medical expenses.

Does homeowner insurance cover mold?

Mold coverage isn’t guaranteed by your homeowners insurance policy. Typically, mold damage is only covered if it’s related to a covered peril. Mold damage caused by flooding would need to be covered by a separate flood insurance policy.

Does homeowners insurance cover window replacement?

If your window needs repair or replacement because it’s drafty, for instance, homeowners insurance will not cover the cost. … Remember, unless the damage is caused by a sudden or accidental peril — hail, fire or theft, for example — it’s likely not covered by homeowners insurance.

Which area is not protected by most homeowners insurance framework?

2. What’s NOT Covered On a Standard Homeowners Insurance … Earthquake and water damage. In most states, earthquakes, sinkholes, and other earth movements are not covered by your standard policy.

What is not covered under medical payments to others?

The choices vary by state and by insurance company, but typically the limit is between $1,000 and $5,000. Pain and suffering and property damage are not covered by medical payments to others coverage.

Which of the following would not be covered under Section II of the homeowners policy?

Which of the following would not be an insured under Section II of the Homeowners Policy? … Property of a roomer, boarder or tenant — Property of roomers, boarders, or tenants is not covered under the policy.

Which person is not a covered resident under the homeowners policy?

A nonrelative living in your home is not eligible for coverage on your policy. Full time students are considered insureds if they are related to you, under 26 years-of-age and were residents of your household before moving out to attend school. Students not related to you are covered until age 21.

What is the most important part of homeowners insurance?

The most important part of homeowners insurance is the level of coverage. Avoid paying for more than you need. Here are the most common levels of coverage: HO-2 – Broad policy that protects against 16 perils that are named in the policy.

How much should my house be insured for?

Most homeowners insurance policies provide a minimum of $100,000 worth of liability insurance, but higher amounts are available and, increasingly, it is recommended that homeowners consider purchasing at least $300,000 to $500,000 worth of liability coverage.

What type of homeowner's insurance coverage should you get?

Most homeowners insurance policies have a minimum of $100,000 in liability coverage. But you should buy at least $300,000—and $500,000 if you can.

How can I pay for my roof with no money?

- Options to Consider.

- Finance Repair Costs. If you can’t afford repairs on your roof, there are several financing options available to help you. …

- Apply for a Grant. …

- Reach out to Your Network. …

- Refinance Your Home. …

- Save the Money. …

- The Roof Doctor is an Affordable Option.

Does home insurance cover cracked walls?

Homeowners insurance will cover foundation repair if the cause of damage is covered in your policy. But damage caused by earthquakes, flooding, and the settling and cracking of your foundation over time are not covered.

Will insurance cover hidden water damage?

Hidden Water Coverage Simply put, it covers the cost to repair damage done by a water leak you can’t see within the walls, floors, ceilings, cabinets, beneath the floors or behind or under a home appliance. A homeowners policy normally doesn’t protect you from many types of water damage — including hidden water leaks.

Is it illegal not to have house insurance?

Legally, you can own a home without homeowners insurance. However, in most cases, those who have a financial interest in your home—such as a mortgage or home equity loan holder—will require that it be insured.

How long can I leave my house unoccupied?

Generally, if you plan to leave your home vacant or unoccupied for 30 days or more, you’ll want to purchase unoccupied or vacant house insurance. While terms vary by policy, most insurance companies will deny claims that are made if your home is left alone for longer than 30 days.